Many practitioners agree that there has been no fundamental change in family law with a greater impact on our daily practice than the elimination of the federal tax deduction on a payer’s alimony obligation imposed by the Tax Cuts and Jobs Act of 2017 (hereinafter, the “Act”).[1] One need only consider the vast number of commentators who opined on the pending change prior to the alimony-related January 1, 2019 effective date, and the number of practitioners who raced to the courthouse to finalize divorces before the new year to see the depths of the uncharted waters before us.

.1).1901281527550.jpg)

With the change having arrived within the matrimonial legal community, we now need to collectively, creatively and quickly adapt to the Act’s newly designed alimony landscape. This article will briefly discuss how the Internal Revenue Code (hereinafter, the “Code”) previously addressed alimony, the Act’s amendments to certain Code-related alimony provisions, and how those amendments impact upon our practice.

- How did the Code previously address alimony?

Prior to the Act,[2] the Code provided that “alimony or separate maintenance payments” were deductible from income by the alimony payer and includible in the recipient’s gross taxable income for that calendar year.[3] An “alimony or separate maintenance payment” was defined as any payment in cash (including checks or money orders) if:

- such payment is received by (or on behalf of) a spouse under a divorce or separation instrument,

- the divorce or separation instrument does not designate such payment as a payment which is not includible in gross income under this section and not allowable as a deduction under section 215,

- in the case of an individual legally separated from his spouse under a decree of divorce or of separate maintenance, the payee spouse and the payer spouse are not members of the same household at the time such payment is made (only if the spouses are legally separated under a decree of divorce or of separate maintenance), and

- there is no liability to make any such payment for any period after the death of the payee spouse and there is no liability to make any payment (in cash or property) as a substitute for such payments after the death of the payee spouse.[4]

A payment could not be deemed alimony if: (1) the spouses filed joint returns with each other; (2) the payment was treated as child support; (3) the payment was voluntarily made and not pursuant to a divorce or separation instrument; (4) the payment was treated as a property settlement; (5) the payment was designed to “keep up” the payor’s property; or (6) the payment was for use of the payor’s property.[5] A “divorce or separation instrument” was defined as:

- a decree (not described in subparagraph (A)) requiring a spouse to make payments for the support or maintenance of the other spouse. This includes a temporary decree, an interlocutory (not final) decree, and a decree of alimony pendente lite (while awaiting action on the final decree or agreement).”[6]

Simply put, so long as a payment could be deemed alimony under the Code, it could be deductible from the payer’s gross income on a federal income return and includible as taxable income on the recipient’s federal income tax returns. The goal of this decades-old system, recently referred to as a “divorce subsidy” by the House Ways and Means Committee,[7] was to further incentivize a payer to pay alimony by lowering the payer’s taxable income. This incentive, however, cost the federal government millions of dollars per year in lost tax revenue as alimony payers presumably paid taxes at a lower tax bracket because of the deduction, while alimony recipients also presumably paid taxes on alimony at a lower tax bracket than the payer would have absent the deduction.[8] Another basis for eliminating the deduction on alimony stemmed from a lack of “checks and balances” whereby alimony was not being properly reported to the I.R.S. on filed tax returns and, as a result, taxes not being appropriately paid.[9]

- How does the Act amend the Code’s alimony language?

As indicated above, the Act eliminated from federal tax returns: (1) the payer’s ability to deduct alimony payments; and (2) the payee’s requirement to include alimony as taxable income. The elimination will provide the federal government with billions of dollars in increased tax revenue as income taxes will be paid only at the payer’s presumably higher income tax rate. The recipient’s lower taxable income may even qualify him or her for certain government benefits that may not have otherwise been available if alimony were still included in the recipient’s gross income.

Section 11051 of the Act – Repeal of Deduction for Alimony Payments, provides that alimony shall no longer be deductible by the payor and includible in the payee’s gross income.[10] Certain notable amendments to the Code are as follows:

- Section 61: “Alimony and separate maintenance payments” are no longer included in the Code’s definition of “gross income.”

- Section 62(a)(10): “Alimony and separate maintenance payments” are no longer deductible from Adjusted Gross Income.

- Section 71: Definition of “Alimony and separate maintenance payments” is stricken.

- Section 682: Elimination of language as to alimony trusts, which provided for the inclusion in the “wife’s” gross income “the amount of the income of any trust which such wife is entitled to receive and which, except for this section, would be includible in the gross income of her husband, and such amount shall not, despite any other provision of this subtitle, be includible in the gross income of such husband.”

- Section 3402(m)(1) and Section 121(d)(3): “Alimony and maintenance payments” are stricken as to the use of property pursuant to a divorce decree or separation instrument.[11]

Notably, with the elimination of the alimony tax deduction also went the oftentimes misunderstood concept of alimony recapture. The recapture rule was designed to prevent situations where a divorce occurs at or near the end of a calendar year and the payer attempts to procure a tax advantage by making a tax-deductible property settlement agreement at the beginning of the following calendar year.[12] Parties now, perhaps, have a greater opportunity to exercise flexibility and creativity in their alimony agreements in a way not previously seen under a potential recapture penalty. Similarly, alimony buyouts no longer must be “tax effected”, and related negotiations need not occur to determine which tax rate should be applied.

- The Effective Date of the Act’s Alimony Amendments.

A primary focus on the Act’s alimony-related amendments, to date, have pertained to the amendments’ effective date. The largely scrutinized language provides that the amendments apply to:

- Any divorce or separation instrument (as defined in section 71(b)(2) of the Internal Revenue Code of 1986 as in effect before the date of the enactment of this Act) executed after December 31, 2018, and

- Any divorce or separation instrument (as so defined) executed on or before such date and modified after such date if the modification expressly provides that the amendments made by this section apply to such modification.

Much of our concern as practitioners, has, thus far, been placed on those divorce or separation instruments “executed on or before” December 31, 2018. Similarly, many practitioners attempted to preserve the alimony tax deduction by entering into Consent Orders addressing alimony on a pendente lite basis before year-end could because I.R.S. Pub. 504 includes in its definition of a “divorce or separation instrument” a “temporary decree, an interlocutory (not final) decree, and a decree of alimony pendente lite (while awaiting action on the final decree or agreement).”[13] While many legal and tax professionals assert that marital settlement agreements signed before January 1, 2019 would not be subject to the Act even if such agreements were not incorporated by the Superior Court into a Final Judgment of Divorce prior to the new year, there remains no definitive answer or guidance from the Internal Revenue Service on this issue as of the date of this article’s completion. It was a result of such uncertainty why trial judges went out of their way to accommodate practitioners and litigants during the holiday season to ensure that as many divorces as possible could be entered and finalized before the clock struck midnight on 2018.

As to divorce or separation instruments “executed on or before” December 31, 2018 and “modified after” December 31, 2018, the Act appears clear that its amendments will only apply to such modification if expressly provided. While one can envision parties negotiating a post-Judgment alimony modification incorporating or declining to incorporate the Act’s amendments, there exists uncertainty as to when and on what basis a trial judge would direct the Act’s amendments to apply.

In addressing alimony, many, if not most settlement agreements executed on or before December 31, 2018 provided alimony was tax deductible on the payer’s federal income tax returns and includible as income on the recipient’s federal income tax returns. Even prior to the Act’s origination, some agreements also provided that a future change in the federal and/or state income tax code would constitute a change in circumstances requiring a review and potential modification of alimony if such change impacted upon the alimony obligation’s tax deductibility.[14] As applicable to the Act, this language may prove unnecessary to the extent the Act states its terms will only apply to a post-effective date modification if the modification expressly provides as such.

Some recent agreements have taken this language a step farther by specifically indicating whether the Act’s terms will apply to a post-effective date modification. If the agreement expressly prohibits any future application of the Act to an alimony modification, one could argue it is incumbent upon a trial judge to implement and enforce the parties’ agreement as written.[15] To the contrary, one could argue that the trial judge should exercise discretion as necessary to ensure a fair and equitable alimony arrangement regardless of tax-based language such as that detailed above.[16]

Another untested issue that will impact upon many litigants is how the Act will impact upon alimony language contained in prenuptial agreements executed before January 1, 2019. The Act makes no mention of prenuptial agreements, many of which expressly define what the payer’s alimony obligation will be or specify a formula by which alimony will be calculated if the marriage terminates. Without language addressing an alimony obligation’s tax deductibility, questions arise as to whether the arrangement is subject to challenge based solely on the Act’s implementation, especially under those agreements executed after New Jersey’s premarital agreement law changed in 2013 to limit challenges of unconscionability to only those existing at the time of an agreement’s execution.[17] While some commentators suggest amending prenuptial agreements to address the change, many spouses will understandably be reluctant to do so mid-marriage, aside from any potential post-nuptial agreement enforceability issues.[18]

Ultimately, practitioners will continue to advocate on this issue as necessary while waiting for the I.R.S. to issue guidance on how the amendments’ effective date will impact upon alimony orders and agreements.

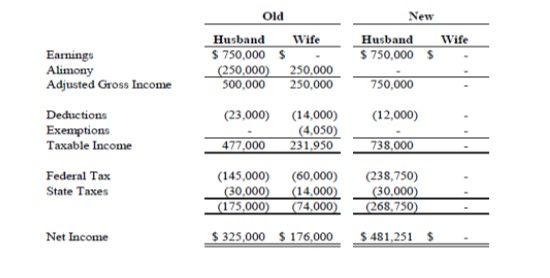

- Basic Example for Illustrative Purposes.

While the alimony payer will no longer receive a federal income tax deduction, he or she will potentially be paying taxes at a lower tax rate than before. By way of example, a single filing payer earning $100,000 under pre-Act law fell within the 28% tax bracket. Under the Act, the tax bracket for the same filing status and income is 24%. Similarly, a head of household filing payer earning $450,000 under pre-Act law fell within the 39.6% tax bracket. Under the Act, the tax bracket is 35%. To that end, under the Act all income levels experience a decrease in their respective tax rates.

The following example illustrates how the tax burden will revert to the payer.[19]

The example shows the substantial increase in taxable income and resulting taxes a payer will have to pay under the Act. Under the pre-Act breakdown, the payer is left with $325,000 in net dollars after funding a net, after tax alimony payment to the recipient of $176,000. Under the Act, the payer would be left with $305,251 to achieve the same net payment to the recipient, which constitutes a six percent (6%) decrease in the payer’s net, disposable income with which to meet all other expenses. The result is substantially less money in after-tax dollars with which to fund an alimony obligation.

- What Happens Now?

The alimony tax deduction was not only an incentive for the payer spouse to pay a greater amount of alimony, but it also proved a useful tool by which attorneys and litigants negotiated alimony settlements. Although not based in statute or case law, many practitioners calculated alimony through a more formulaic approach largely dependent on parties’ incomes and resulting tax consequences. In so doing, however, the importance of the marital lifestyle, related need and all other requisite statutory alimony factors were often minimized.[20]

Absent a new formulaic approach, practitioners will be more compelled to rely upon the alimony statute. Put another way, the litigation and settlement of alimony disputes may more closely resemble each other than that previously experienced and be more akin to how we often address higher income matters. A determination of lifestyle will stand at the forefront with forensic accounting experts potentially taking on a greater role in addressing the parties’ respective incomes and resulting tax consequences in fashioning an alimony award, and the impact of alimony on the parties’ lifestyles and resulting needs.

As a general principle, the law provides alimony should be set at an amount that will “enable each party to live a lifestyle ‘reasonably comparable’ to the marital standard of living.”[21] Most commentators agree the amended statute codified the central holding in Crews and its progeny by requiring a consideration of “The standard of living established in the marriage or civil union and the likelihood that each party can maintain a reasonably comparable standard of living, with neither party having a greater entitlement to that standard of living than the other.”[22] The statute also provides:

Determination of the length and amount of alimony shall be made by the court pursuant to consideration of all of the statutory factors set forth in subsection b. of this section. In addition to those factors, the court shall also consider the practical impact of the parties’ need for separate residences and the attendant increase in living expenses on the ability of both parties to maintain a standard of living reasonably comparable to the standard of living established in the marriage or civil union, to which both parties are entitled, with neither party having a greater entitlement thereto.[23]

Considering the tax consequences to both parties in rendering an alimony award and, in connection therewith, determining whether the “reasonably comparable” lifestyle can be met for both parties is a required statutory factor in the trial court’s analysis. Factor twelve (12) in the statute requires consideration of “The tax treatment and consequences to both parties of any alimony award, including the designation of all or a portion of the payment as a non-taxable payment.”[24] Unless the trial court expressly finds otherwise, the resulting tax consequences must be considered equally with all other statutory factors. This factor is also a potential “exceptional circumstance” under the statute for adjustment to the alimony duration.[25]

Thus, in rendering an award, the seminal cases of Crews[26] and Hughes[27] require the trial court to first identify the marital lifestyle and then determine to what extent the “reasonably comparable” standard can be met for both parties on a going forward basis. A trial judge can be as creative as before to achieve a fair and just result, and as part of such creativity account for the parties’ respective tax consequences and formulate an alimony award in a way that makes equitable sense.[28] One could argue that the trial judge has even greater flexibility than before, especially as it pertains to the interrelationship between alimony and equitable distribution. As indicated above, the same can arguably be said for practitioners seeking to achieve settlement.

- Conclusion

While the elimination of the federal income tax deduction for alimony has left matrimonial practitioners somewhat uncertain as to what the future holds, a consideration of the alimony landscape in its entirety demonstrates that this latest change provides attorneys with another opportunity for creative lawyering and trial judges with what is, perhaps, a greater ability to fashion more fair and equitable awards for litigants.

[1] The author is a Partner at Ziegler & Resnick LLC and a member of the New Jersey State Bar Association, Family Law Executive Committee. He expresses his great appreciation to all those who provided their thoughts and feedback on this article.

[2] Tax Cuts and Jobs Act of 2017, Pub. L. 115–97 (2017).

[3] The author acknowledges that the existing Code provisions still apply to alimony obligations preceding the Act’s effective date as to the deduction elimination and references such provisions in the past tense in a manner consistent with the Act’s amendment scheme.

[4] 26 U.S.C. Secs. 215 (2018). The I.R.S. provided under Topic No. 452:

If youpaid amounts that are considered alimony, you may deduct from income the amount of alimony you paid whether or not you itemize your deductions. Alimony payments are only deductible on Form 1040.pdf, U.S. Individual Income Tax Return.

. . .

If you received amounts that are considered alimony, you must include the amount of alimony you received as income. You may only report alimony received on Form 1040, or on Schedule NEC, Form 1040NR.pdf, U.S. Nonresident Alien Income Tax Return.

[5] 26 U.S.C. Sec. 71 (2018).

[6] Id.

[7] See I.R.S. Pub. 504.

[8] PBS New Hour, How the tax overhaul will affect alimony deductions, Jennifer Peltz, Associated Press, https://www.pbs.org/newshour/politics/how-the-tax-overhaul-will-affect-alimony-deductions (last viewed December 30, 2018). According to the article, the Internal Revenue Service reported that 361,000 taxpayers “claimed they paid a total of $9.6 billion in alimony in 2015, though only 178,000 reported receiving spousal support.”

[9] See id. According to Congress’s non-partisan Joint Committee on Taxation, the deduction elimination will add $6.9 billion in new tax revenue over the course of the next decade. While this is undoubtedly a large sum of revenue gained, it equals less than half a percent of the $1.5 trillion tax cut plan implemented by the Act.

[10] See id.

[11] See Tax Cuts and Jobs Act of 2017, supra, Section 11051.

[12] See id.

[13] See I.R.S. Pub. 504. A payer could be subject to “recapture” if alimony payments “decrease substantially” or end during the first three (3) calendar years following the obligation’s commencement. Pursuant to the Code, “decrease substantially” meant either: (1) the alimony amount paid in the third year plus fifteen thousand dollars ($15,000) was less than the alimony amount paid in the second year; or (2) the average of alimony payments made in the second and third years plus $15,000 was less than alimony paid in the first year. If subject to recapture, the payer had to include in the third year’s taxable income any “excess alimony” paid during the first and second years, while the recipient could deduct that same amount in the third year. In so doing, it essentially balanced out for the recipient taxes paid on the first two (2) years of alimony.

[14] See I.R.S. Pub. 504.

[15] See generally Lepis v. Lepis, 83 N.J. 139, 149 (1980).

[16] Harrington v. Harrington, 281 N.J. Super. 39, 46 (App. Div. 1995) (citing Lahue v. Pio Costa, 263 N.J. Super. 575 (App. Div. 1993), certif. denied, 134 N.J. 477 (1993) (quoting Pascarella v. Bruck, 190 N.J. Super. 118, 125, (App. Div. 1983), certif. denied, 94 N.J. 600 (1983); Bistricer v. Bistricer, 231 N.J. Super. 143, 147 (Ch. Div. 1987); Davidson v. Davidson, 194 N.J. Super. 547, (Ch. Div. 1984)).

[17] See Lepis, supra, 83 N.J. at 149.

[18] See N.J.S.A. 37:2-38 (2018).

[19] See Pacelli v. Pacelli, 319 N.J. Super. 185 (App. Div. 1999).

[20] The author thanks Kevin Baldwin, CPA/ABV of David Landau & Associates for providing the above-chart for inclusion in this article.

[21] N.J.S.A. 2A:34-23b.

[22] Crews v. Crews, 164 N.J. 11, 26 (2000) and the Crews citation to N.J.S.A. 2A:34-23(b)(4)).

[23] N.J.S.A. 2A:34-23b

[24] Id.

[25] Id.

[26] Id.

[27] Crews, supra, 164 N.J. at 26.

[28] Hughes v. Hughes, 311 N.J. Super. 15 (App. Div. 1998).

[29] Lepis, supra, 83 N.J. at 149.